What Is a CBDC?

A CBDC, or Central Bank Digital Currency, signifies a digital form of a country's fiat currency, essentially representing a virtual version of a specific nation's coinage. Issued and regulated by a nation's central bank, a CBDC acts as legal tender, just like conventional money. A major benefit of a CBDC is that it enhances transaction efficiency while minimizing the cost associated with creating, storing, and distributing physical money.

How Does a CBDC Work?

CBDCs operate similarly to cryptocurrencies; they use a digital or tokenized version of the nation's coinage. The million-dollar question is: does CBDC use blockchain? The answer is yes, and no. While some countries may employ blockchain technology, others may prefer to use a digital ledger that isn't specifically blockchain but works on equivalent principles.

CBDC vs. Fiat Currency

CBDCs are a response to the changing landscape of finance, offering a digital alternative to physical cash and traditional banking systems. They modernize the financial infrastructure by enabling faster and more efficient digital transactions, reducing the reliance on physical currency.

Enable Easier Digital Transactions

CBDCs can potentially render many fiat currency attributes into the digital sphere. They can improve the speed, safety, and cost-efficiency of transactions. Yet, their digital nature suggests they might not be usable in instances where traditional cash reigns supreme, like in remote areas with limited digital infrastructure.

Improve Financial Inclusion

CBDCs can improve financial inclusion by providing access to digital financial services for individuals and businesses who may not have access to traditional banking. They promote broader participation in the formal economy, especially in regions with limited banking infrastructure.

Enhance Payment Systems

CBDCs can enhance payment systems by offering a secure, instant, and cost-effective means of transacting. They reduce the reliance on intermediaries like payment processors and banks, potentially lowering transaction costs.

What Does CBDC Mean for Banks?

CBDCs offer central banks new tools for implementing monetary policy. They can influence the money supply, interest rates, and inflation, providing greater control over the economy's stability.

CBDCs could redefine the role of banks as intermediaries, altering their importance in monetary systems. It's also plausible that CBDCs might lead to tighter regulations and oversight from central banks. In addition, their digital infrastructure reduces transaction costs and time, potentially impacting banks' roles in processing remittances and payment transfers.

CBDC vs. Crypto: Understanding the Differences

While CBDCs and cryptocurrencies are digital currencies, their centralization, regulatory framework, user privacy, and underlying technology differ significantly. These distinctions impact their intended purposes, use cases, and acceptance within the financial ecosystem. Here are some of the key differences between CBDCs and cryptocurrencies:

Centralization vs. Decentralization

CBDCs are issued and regulated by central banks, with complete control over the issuance, supply, and management. Central banks can maintain monetary stability and implement monetary policies within the existing financial system while issuing CBDCs.

On the contrary, cryptocurrencies operate on decentralized networks with no central authority. Blockchain technology allows peer-to-peer transactions without the need for intermediaries.

While theoretically decentralized, some aspects of cryptocurrency can become centralized through, for example, using an exchange to buy or store the coins. CBDCs, although fundamentally centralized, may accommodate decentralization to some extent by giving people more privacy and power over transactions.

Stability and Value

The value of CBDCs, based on a nation's fiat currency, remains stable, making them suitable for everyday transactions. In comparison, cryptocurrencies such as Bitcoin and Ethereum are known for their value volatility, influenced by market demand and speculative factors. This can present investment opportunities but also makes their use in daily transactions risky.

Privacy and Anonymity

The level of privacy can vary with CBDCs. Some designs of CBDCs might prioritize transaction privacy, while others could enable audit features to manage regulatory oversight and prevent illicit activities.

On the contrary, cryptocurrencies are often associated with pseudonymity. However, despite the perceived anonymity, blockchain analysis techniques have been known to reveal user identities.

Primary Use Cases

CBDCs are typically created for national economic and regulatory purposes, such as improving financial inclusion and streamlining cross-border transactions. On the other hand, cryptocurrencies were originally developed as an alternative to traditional financial systems.

CBDC vs. Cryptocurrency: A Breakdown

|

CBDC |

Crypto |

|

|

Features |

- Digital form of a government-issued currency. - Centralized and operated by the state. |

- Decentralized digital currencies leveraging blockchain technology. |

|

Benefits |

- Convenience of digital transactions. - Central regulation potentially reduces threats of volatility and fraud. |

- Enables peer-to-peer transactions without the need for an intermediary. - Potential for high returns due to market volatility. |

|

Challenges |

- Risk of cybersecurity threats. - May not be usable in areas with limited digital infrastructure. |

- Highly volatile leading to potential financial loss. - Regulatory and legal issues differ per region. |

|

Noted Examples |

- China's e-CNY - Eastern Caribbean's DCash - Jamaica's JAM-DEX |

- Bitcoin - Ethereum |

CBDC vs. Stablecoins: How Is a CBDC Different From a Stablecoin?

Stablecoins, like CBDCs, represent a form of digital currency. However, while CBDCs are issued by central banks, stablecoins are issued privately, such as PayPal's stablecoin PYUSD, to facilitate a blockchain initiative. Stablecoins are designed to minimize volatility through the backing of reserve assets and offer investors a safer way to earn passive income, especially during bearish market conditions.

Which Countries Have CBDCs?

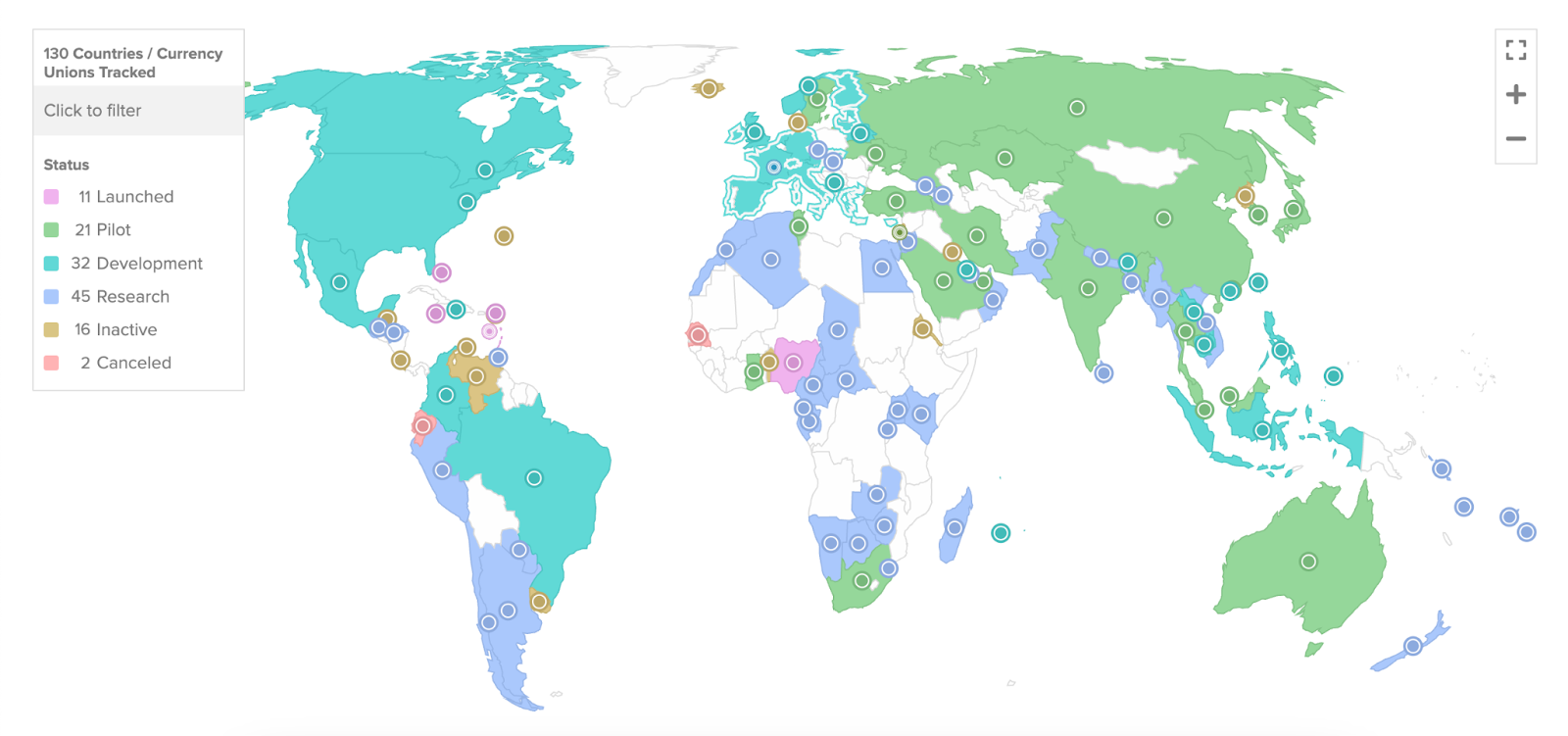

From around 35 countries considering CBDCs in May 2020, the number has now shot up to 130 countries worldwide, according to data from Atlanta Council. 19 of the G20 nations are in the advanced stages of developing their respective CBDCs.

As of now, several countries, like China (digital yuan), Bahamas (Sand Dollar), and Nigeria (eNaira), have advanced prominently in the CBDC realm. Other countries, including the USA (FedNow), are at various CBDC development and exploration stages.

Progress on CBDCs Across the World | Source: Atlantic Council

Here are some countries and their progress on CBDC projects as of August 2023:

The Bahamas

The Central Bank of The Bahamas issued the Sand Dollar in October 2020, making it the world's first nationwide CBDC. The Bahamas' use of a functioning blockchain ecosystem indicates its commitment to modern financial technology. The Sand Dollar has been crucial in solving transaction difficulties faced by The Bahamas, particularly after natural disasters like Hurricane Dorian in 2019. The first CBDC worldwide is also one of the most advanced national digital currencies globally.

Australia

Australia's Commonwealth Bank and ANZ Banking Group are part of the Reserve Bank of Australia's pilot program to explore the eAUD, a CBDC. They are testing its use cases alongside other financial institutions and payment companies.

Brazil

Brazil's CBDC has been officially named "DREX." The Central Bank of Brazil unveiled a pilot program for its CBDC, the digital real, with the final rollout expected by the end of 2024. This pilot utilizes distributed ledger technology (DLT) and is designed to settle wholesale interbank transactions.

China

China made history by launching its digital yuan or e-CNY nationwide during the 2022 Beijing Winter Olympics, becoming the first major economy to do so. It represents a significant milestone in adopting digital currencies at the national level. China has ambitious plans to take its digital yuan beyond its borders, aiming to bring it to a broader global stage. This initiative could expand the use of the digital yuan on an international scale.

India

The Reserve Bank of India (RBI) launched a pilot for its CBDC in the retail segment, issuing a concept note and pilot in October 2022. India has plans to launch its central bank digital currency at a national level by the end of 2023. By June 2023, more than 1.3 million users had downloaded the CBDC wallet, and around 300,000 merchants had started accepting CBDC payments.

Will CBDC Replace Cryptocurrency?

Similarly, replacing decentralized cryptocurrencies would catch fundamental contradictions, given their differing ideologies. While CBDC aims to regulate control over financial transactions, cryptocurrency's allure often lies in its decentralization and absence of regulatory authority.

As we enter the digital future of money, the puzzle around CBDCs becomes clearer and more fascinating. From being aspirational to the potential of becoming transactional in our daily lives, CBDCs are much more than a simple digital echo of existing money—they could be a powerful tool for financial evolution and financial inclusion.

Will CBDC Replace Cash?

Although CBDCs offer numerous benefits, factors such as digital literacy, privacy concerns, and cyber security issues make it unlikely that CBDCs will replace cash entirely in the near future.

Closing Thoughts

The topic of Central Bank Digital Currencies (CBDCs) is one of keen interest in today's digital and financial world. Considering the current trends, CBDCs may not fully replace cash or cryptocurrencies anytime soon. Still, they could work together to offer more diverse, efficient, and secure monetary systems.

While cryptos offer decentralization and fiat currencies provide stability, CBDCs, and stablecoins balance central control with digital convenience. However, like all financial systems, they aren't devoid of challenges, from technical infrastructure to regulatory oversight.

In this digital paradigm, these variations - CBDCs, stablecoins, cryptocurrencies, and fiat currencies - fuel our global financial engine. As we move forward, it's intriguing to envision how these monetary systems will co-evolve, potentially revolutionizing our financial future. Regardless of how they evolve, one thing's for sure - the future of money is not just digital; it's diversified.